Why Mortgage Lending Is Finally Ready for AI Voice Agents

Mortgage's Voice Era

Why lending is finally AI-ready

The mortgage industry has spent 20 years trying to solve the same problems with incrementally better tools. None of them worked. AI voice agents are changing that.

The Shift Nobody Was Ready For

For most of its history, mortgage was a relationship business. Loan officers worked their local markets, knew their borrowers by name, and closed deals over handshakes and kitchen tables.

Then the aggregators arrived. LendingTree, Zillow, Bankrate—suddenly a borrower could submit one form and have five lenders competing for their business simultaneously. The game shifted from relationships to speed and volume overnight, and most mortgage operations never fully adapted.

The 2008 crash made things worse in a different way. Dodd-Frank, the creation of the CFPB, and TILA-RESPA integrated disclosures added layers of compliance overhead that permanently raised the cost of originating a loan. Lenders needed more staff to stay legal, let alone grow.

By the mid-2010s, the industry was stuck: higher lead costs, more competition per lead, more compliance burden per loan, and the same fundamental operational model—humans calling humans—underneath all of it.

The Band-Aid Era: 2013–2022

The mortgage tech boom promised to fix this. CRMs got smarter. Power dialers got faster. Chatbots appeared on websites. Lead routing tools promised to get the right lead to the right loan officer at the right time. Automated email drips kept borrowers "engaged."

What happened: loan officers got more dashboards to look at and more tools to manage, but the core problems didn't move. Leads still went cold because no tool could make a human pick up the phone at 10 PM on a Saturday. Document collection still stalled pipelines because automated emails asking for pay stubs have a 15 percent response rate. Inbound calls still hit voicemail during lunch breaks and after hours.

Then the 2020–2021 refi boom exposed every crack. Mortgage rates dropped below 3 percent for the first time in history, origination volume exceeded $4 trillion, and lenders hired aggressively to keep up. When rates doubled to more than 6 percent through 2022, volume collapsed almost overnight. Lenders of every size—from the largest online originators to regional shops—cut tens of thousands of jobs industry-wide.

You can't staff your way out of a structural problem. The cycle repeats because the underlying model—every borrower interaction requires a human—never changed.

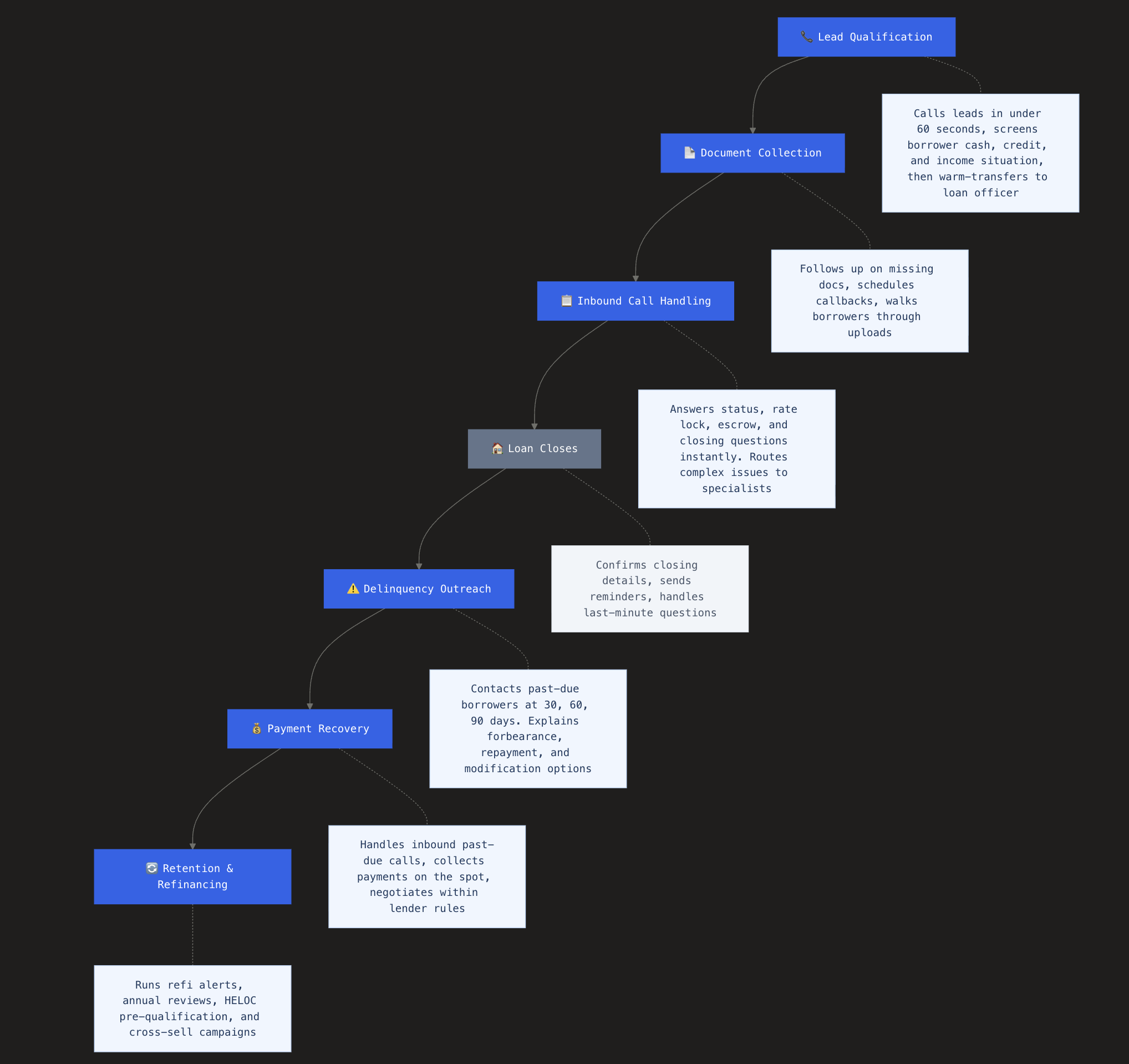

Image: AI voice agent touchpoints across the mortgage borrower lifecycle

How Voice AI Is Revolutionizing Mortgage Lending

The tools from the band-aid era automated workflows around humans. AI Voice Agents automate the conversations themselves, a structural change in how mortgage operations work.

Conduit AI is the Conversational AI platform built for exactly this shift—deploying Voice Agents and Chat Agents across every channel to handle conversations autonomously while keeping humans in the loop for complex scenarios.

Voice Agents show up across the lifecycle:

Lead Qualification and Speed to Lead

A borrower fills out a rate comparison form at 9:30 PM. They've submitted to four lenders. Within 30 seconds, the AI Voice Agent calls—while the form is still fresh in the borrower's mind. The agent runs a natural qualification conversation: credit score range, property type, purchase or refinance, down payment, employment status, and loan amount. The questions adapt based on answers—a self-employed borrower gets different follow-ups than a W-2 employee.

If the borrower qualifies and wants to proceed, the agent warm-transfers them to a loan officer with full context: credit profile, property details, timeline, and intent level. If it's after hours, the agent books a callback for the next morning, confirms via text, and calls the borrower at the scheduled time to reconnect them with an LO.

For leads that don't convert on the first call, the agent runs a structured nurture sequence over 30–45 days—calls, texts, and emails with multiple touchpoints, all within TCPA and state-specific calling limits. No lead sits unworked in the CRM.

Contact rates move from the 10–15 percent industry average to 30–50 percent. Loan officers stop dialing through cold lists and start picking up live, pre-qualified conversations. For more on why the first five minutes determine who gets the deal, see our speed-to-lead guide for loan officers.

Document Collection and Pipeline Acceleration

A loan application is moving through processing, but the file is stuck. Two documents are missing—a bank statement and a signed disclosure. The processor has sent a couple of emails without a response.

The AI Voice Agent calls the borrower directly: "Your loan application is moving forward—we need two items to keep things on track." The agent names the specific documents, explains what's needed, and offers to walk the borrower through the upload process right then. If the borrower can't do it immediately, the agent schedules a specific follow-up—"I'll call you at 6 PM tonight"—confirms via text, and calls back at exactly that time.

Processors juggling 30–50 files can't maintain that follow-through at scale. Loans that would have stalled in processing for days over a missing pay stub move forward the same evening. Shorter time-to-close, fewer rate lock extensions, and processors focused on exceptions instead of chasing paperwork.

Inbound Call Handling

A borrower calls the lender's line at noon. The team is at lunch, on other calls, or in a meeting. Instead of voicemail, the AI Voice Agent picks up immediately.

The borrower wants to confirm their closing costs and check whether their rate lock expires before their scheduled closing date. The agent pulls the information from the loan system and answers in real time. For more complex questions—disputing an escrow estimate, asking about a loan modification—the agent collects the details, creates a case, and schedules a callback with the right specialist, confirming the appointment via text.

Routine inquiries get resolved in minutes without a human touching them. Complex issues get routed with full context so the specialist isn't starting from scratch. Voicemail rates drop from 30–40 percent to under 5 percent. Organizations that reduce support costs with AI agents across voice and messaging report 40–60 percent reductions in communication costs.

Delinquency Outreach and Loss Mitigation

A borrower misses their 30-day payment. Instead of a letter that sits unopened on the counter, the AI Voice Agent makes a proactive call. The agent notifies the borrower about the missed payment, explains the available options—forbearance, repayment plans, loan modification—and asks about their situation.

If the borrower is experiencing hardship, the agent collects preliminary details: reason for hardship, current income, and timeline expectations. Then the agent schedules them with a loss mitigation specialist who already has the full picture—no cold handoff, no repeating the story. If the borrower simply forgot, the agent walks them through payment options on the spot.

The outreach runs systematically across the entire 30/60/90-day past-due portfolio. Early intervention contact rates jump from 15–20 percent to 45–55 percent, directly reducing default rates and loss severity—metrics that matter to every servicer and investor. Companies using AI Voice Agents for financial services outreach are already seeing three to four times contact rate improvements over human teams.

The Numbers

| Metric | Industry Average | With AI Voice Agents |

|---|---|---|

| Lead response time | 4–7 hours | Under 60 seconds |

| Lead contact rate | 10–15% | 30–50% |

| Document follow-up cycle | Days | Hours |

| Inbound calls to voicemail | 30–40% | Under 5% |

| Delinquency contact rate | 15–20% | 45–55% |

Source: Based on Conduit AI customer data and industry benchmarks.

Why Now

Two things changed that make this moment different from every previous wave of mortgage tech.

First, the AI is good enough. Voice Agents today handle interruptions, follow-up questions, complex borrower scenarios, and natural conversation flow. They don't sound like a phone tree. Two years ago, this wasn't true.

Second, the economics demand it. Mortgage margins are compressed, lead costs keep rising, and the industry has learned the hard way that headcount doesn't scale with volume. Lenders need a model where capacity isn't tied linearly to people—and AI is the first technology that delivers that. The firms moving fastest are building real-time customer context into their operations so every conversation starts with intelligence, not guesswork.

The lenders who move on this now will build a structural cost advantage that compounds over time. The ones who wait will keep cycling through the same hire-and-cut pattern they've been stuck in for a decade. Understanding how speed to lead differs for purchase versus refinance leads is a practical starting point.

Stay in the loop

Get the latest on AI automation, product updates, and customer stories.